What happens to the rights of policyholders in cases where their death does not lead to termination of the contract?

In a life insurance policy, the policyholder and the insured can be different people. While this configuration may seem strange and even unheard of in certain jurisdictions, the structure is indeed theoretically possible and can be effective when it comes to estate services.

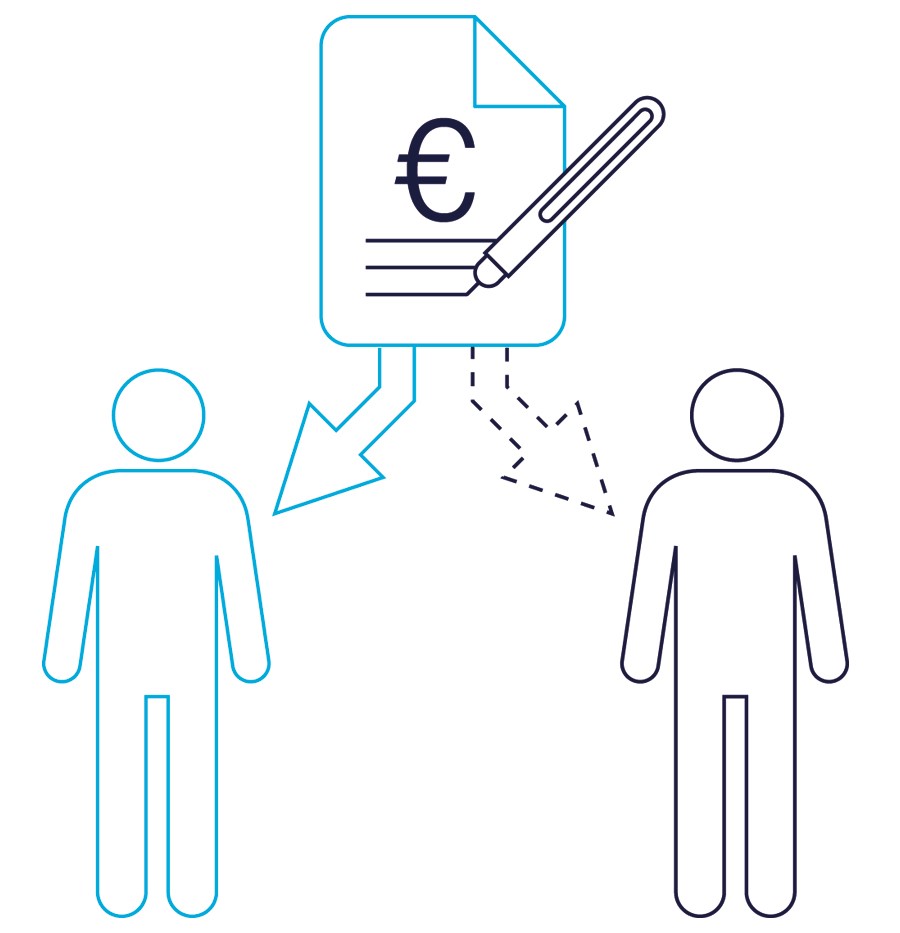

The early death of the insured raises no disputes. However, there is a very different discussion if the policyholder should die first. What becomes of the rights held by the policyholder, and who will be able to exercise them in future? Who will go on to manage the policy, implement surrenders or even amend the beneficiary clause?

Reflecting on the cross-border structure, we have carried out a study of our key markets.

Belgium and the Grand Duchy of Luxembourg have adopted an identical but very complex position. If the policyholder’s rights are not extinguished upon their death, the policyholder’s successors in interests will not inherit the right to revoke the beneficiary clause, the basis of the policy tied to the policyholder. Consequently, exercising other rights cannot undermine a third party stipulation sought by the deceased policyholder. This means that the action taken by the successors in interests is limited to managing the policy, that they are unable to dispose of the policy in any way until its termination. On the other hand, the policyholder has the option to make provisions for all or part of their rights to be transferred, upon their death, to a person of their choice who will be able to exercise all the assigned rights in future. Note that in Luxembourg this assignment is subject to authorisation by the insured.

In France, the legal process is uncertain, as there are no explicit legal provisions. There are two contradictory sets of legal theory. One considers the rights to the policy to be personal and non-transferrable. Consequently, when the applicant dies before the insured, the rights of the applicant die with them and the policy is blocked until the death of the insured. Others consider the applicant’s receivables as ordinary receivables that can be transferred to their heirs as part of their estate like any other estate assets. With no clear position on the subject, the application is made principally, or exclusively, for the lifetime of the applicant(s).

In Portugal, the status of the policy is somewhere between what applies in France on the one hand, and in Belgium and the Grand Duchy of Luxembourg on the other. The rights of the deceased policyholder are not transferred to their heirs and the policy is frozen, unless provisions for a post-mortem assignment were made by the policyholder.

Finland, Denmark and Sweden opted, in this configuration, for a transfer of rights to the beneficiaries who then become the new policyholders.

In the United Kingdom, it is the policyholder’s heirs who inherit the rights in the event of the policyholder’s early death, and who become the new policyholders. However, it is not possible to appoint an assignee in the event of death.

This study shows that the civil consequences of the same structure can be completely different from one jurisdiction to the next. Not to mention the fiscal impact that could affect policyholders’ heirs, assignees and beneficiaries, sometimes through no fault of their own, in such a situation.

Our aim is once again to focus on fully understanding how an insurance policy works before seeking any solution. While a policy can be adapted to bring it in line with another jurisdiction, amending a policy that was badly structured in the first place may prove to be mission impossible. The policyholder then has no choice but to surrender the policy and bear the financial consequences of this surrender.