The accretion clause is, in legal jargon, defined as an onerous commutative and aleatory contract. As the contract presupposes at least two parties, it follows that the survivor has the chance to acquire something under the condition precedent of the co-contracting party’s death. The majority of legal literature states that the accretion agreement is based on two balanced conditions precedent.

The reason for this is simple: each party to the agreement assigns to the co-contracting party their joint interests in a (movable or immovable) property under the condition precedent of their predecease.[1] Consequently, when a specific event occurs (we will be talking about death in the context of this contribution), the share of one of the (predeceased) joint owners shall be acquired ex lege by the second.[2] The chances of gain and of loss of each of the joint owners depend on an uncertain future event, which is beyond the control of the parties.[3] This uncertainty lies not in the death of the co-contracting parties (a certain future event) but in the chronological order of the deaths of the joint owners.

It should be noted that, logically, the accretion clause implies the pre-existence of a joint ownership, i.e. jointly-owned property acquired by spouses married under the regime of separation of property. [4] For an application to life insurance, this criterion will naturally lead us towards a joint application.

As a reminder, a joint application for a life insurance policy implies a joint ownership created between the various policyholders of the same life insurance policy. In fact, the personal rights to the contract (attached to classification as a “policyholder” in the life insurance policy), i.e. right of redemption, right to change the beneficiary clause, arbitration[5], shall be exercised jointly by the joint applicants. This accretion agreement is independent from the legal practice on which it is based. Consequently, it may be entered into after conclusion of a life insurance policy, for example.

1. Legal conditions governing the validity of an accretion clause

As stated above, the accretion clause is an onerous commutative and aleatory contract. We may therefore deduce from this the conditions governing the validity of said clause.

- Onerous agreement: Article 1106 of the Civil Code states: “the onerous contract is that which subjects each of the parties to give or to do something”.[6] We may therefore conclude that each of the parties receives a reciprocal “chance” to receive something (the other’s undivided share). This classification as an onerous agreement is important, as it thus avoids classification as a gift (which would then be potentially restored to the succession and subject to reduction when a question of succession arises).

- Aleatory agreement: the aleatory and commutative nature of the agreement is considered as a sort of equality of opportunity, for each of the parties, to gain wealth. The conditions governing loss or gain in this sort of “gamble” must therefore be equivalent for each of the parties. Consequently, this implies:

- That the contribution of each of the parties must be equivalent

- That the chances of survival of each of the parties must be equivalent.

What happens if there is economic imbalance between the parties’ investments? It is recognised that such an imbalance does not call into question the uncertainty underlying any accretion agreement provided that the parties have equal chances at the outset. This is determined in light of actual circumstances, and therefore involves compensation. Is that feasible? A distinction should be made according to the region in question.

- In the Brussels and Wallonia regions, this compensation is entirely feasible. Case law precedent, which is flexible in such matters, seems to allow it.[7]

- In the Flemish region, VLABEL’s standpoint of 8 January 2018 states that life expectancy as well as one’s own contribution are concepts that cannot be compensated for. As this standpoint is open to criticism, security wants it to be respected in order to avoid any dispute.[8] Any request by the client to go against this standpoint in FLANDERS shall be subject to an analysis by and information from an external specialist consultant.

2. Accretion clause taxation – VLABEL version

With jurisdiction over inheritance tax and certain registration duties since 1 January 2015, the Flemish Region (Vlaamse BelastingDienst or “VLABEL”) is responsible for determining, auditing and collecting or refunding inheritance taxes and registration duties. VLABEL’s jurisdiction is based on the establishment, in the Flemish Region, of the tax residence of inhabitants of the Kingdom or, regardless of the tax residence of the concerned taxpayer, of a real estate property.

The issue that is of particular interest to us at this stage is the application, or otherwise, of Flemish inheritance taxes in the context of a joint life insurance policy (last-to-die configuration) with an accretion of the surviving policyholder’s rights (from the share of the predeceased’s policyholder’s rights) upon the first death. In various decisions, VLABEL has explicitly acknowledged that the accretion agreement is proving to be an effective tool in the context of inheritance optimisation, confirming the non-taxable nature of an accretion for rights relating to a life insurance policy.[9] However, VLABEL does not agree with regard to the sums assigned to the surviving policyholder in return for these rights, i.e. as soon as an insurance benefit occurs (redemption or liquidation of the policy). Consideration should therefore be given to the very basis of this standpoint of VLABEL: the distinction between the rights obtained under the (onerous) life insurance policy and the sums required by virtue of the exercise of these rights (exercise of the right of redemption which would be free of charge). Here is the source of the problem, and the majority of legal literature also disputes this distinction, which is described as artificial. By applying the law literally, there should be no taxation in the situation referred to provided that the accretion agreement is valid.

VLABEL has made a number of contrary decisions, and an official written confirmation would be desirable on this subject. This would put an end to any controversy.

For more information on this subject, please do not hesitate to contact our experts.

Nicolas MILOS – Senior Wealth Planner

[1] See the contributions on this subject of M. VAN MOLLE, D. MICHIELS, F. WERDEFROY or H. CASMAN.

[2] H. CASMAN, Notarieel Familierecht, Gand, Mys & Breesch, 1991, p. 183.

[3] Articles 1104 and 1164 of the Civil Code.

[4] E. DE WILDE D’ESTMAEL, “Appendix 2 – Accretion, survivor’s benefits and hotchpot clauses in the context of gifts of transferable securities”, in Les droits de succession et les droits de donation (Inheritance and Gift Taxes), Brussels, Larcier, 2014, p. 240.

[5] Article 169 et seq. of the law of 4 April 2014 on insurance, M.B. 30/04/2014.

[6] Article 1106 of the Civil Code, in force on 13/09/1807.

[7] Antwerp, 10/02/1988, T. Not., 1989, p. 320, Rev. Not. b., p. 437; Civ. Turnhout, 7/01/2005, C.A.B.G., 2006/6, p. 60.

[8] VLABEL, Standpunt No. 17044.

[9] See inter alia advance ruling BB 17046 of 19 February 2018.

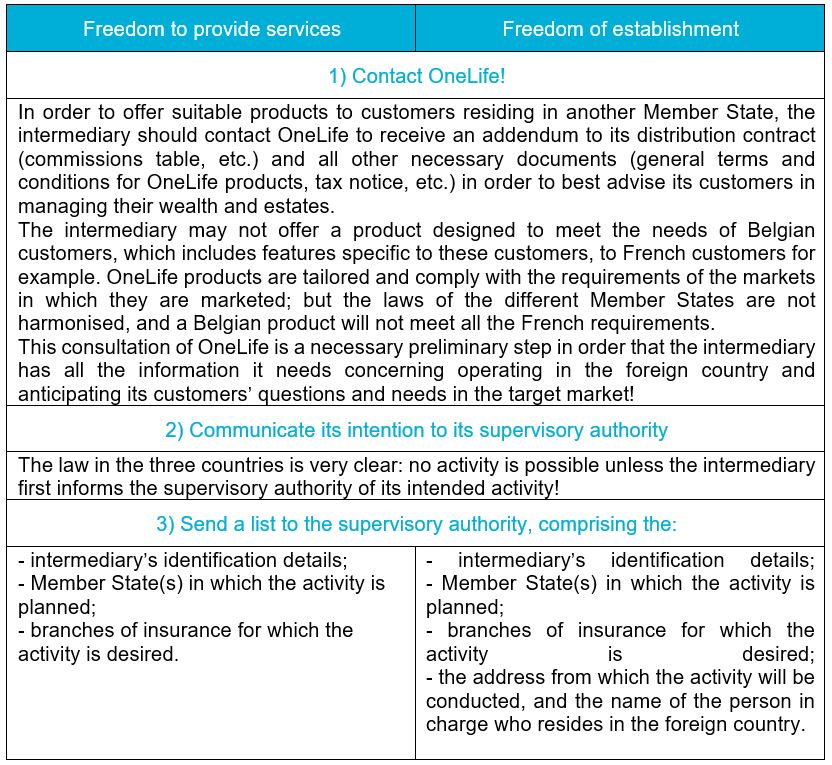

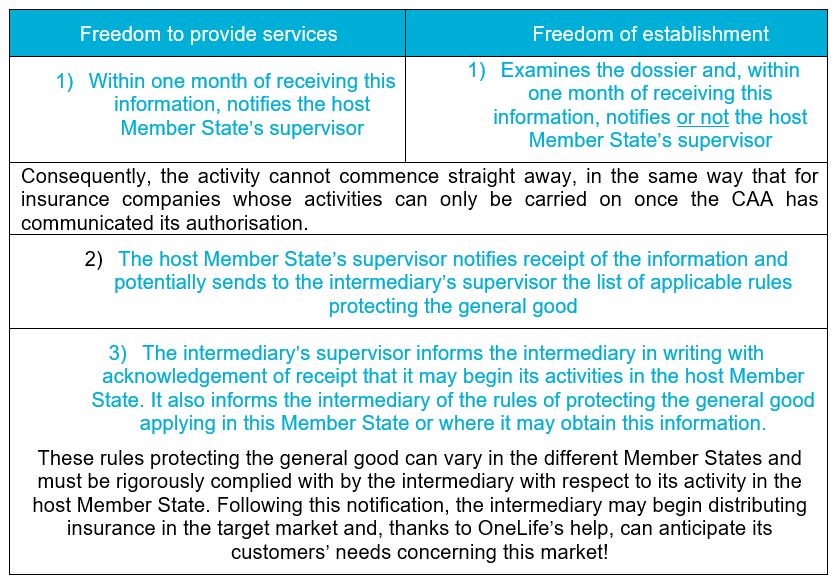

1. Freedom to provide services

1. Freedom to provide services