This topic, which is complex for many wealth managers, is more current today than ever. The challenges to be met – a unique family model for each of our clients (recomposed families, etc.) with an international dimension – are many.

One only has to look at recent news (such as the Jarre or Hallyday affairs) to realise how many problems these two components of a unique family model and an international dimension can cause. Not to mention the lengthy judicial proceedings initiated by the heirs to determine the law applicable to the inheritance.

Is life assurance an ideal solution for passing on an estate?

The advantage of an investment within a life assurance product from a Luxembourg insurance company is that it enables your assets to be managed and passed on totally serenely and in a highly flexible way.

Why Luxembourg?

For its international expertise and a “tailor-made” solution allying clients’ personal and financial situation.

Also for its fiscal neutrality, in particular in respect of inheritance tax.

Our experts will accompany you to enable you to draw up your inheritance solution.

Inheritance rules and practical application: how does this work?

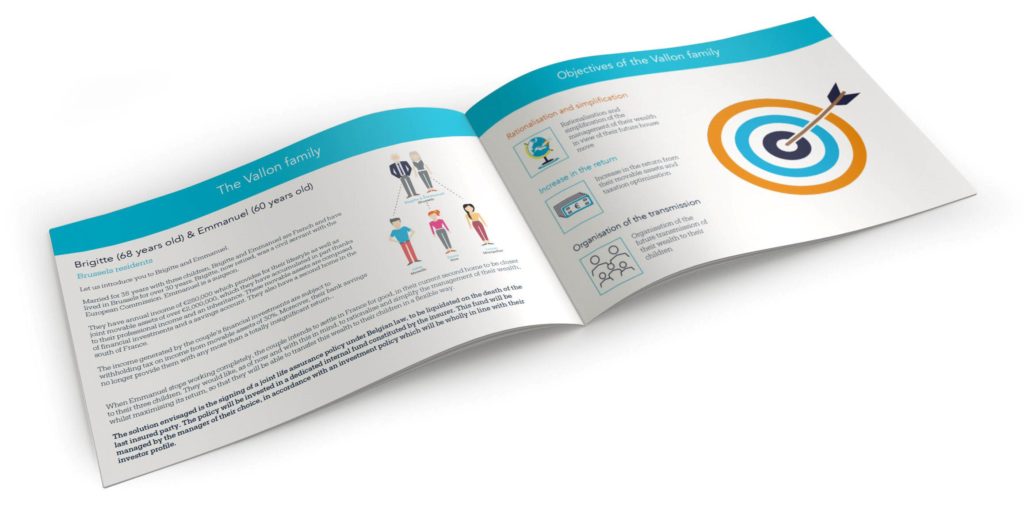

Let us take the example of a French couple married under the regime of wholly shared assets and close to retirement with an integral attribution clause and a capital of €2 million in assets.

They wish to plan their inheritance for their three children – Jean, who lives in Sweden, Paul, who lives in Portugal, and Jeanne, who lives in Belgium.

As a Luxembourg life insurance company, the couple will be advised to take out a joint life assurance policy governed by French law to be redeemed upon the death of the second party.

After the death of the first insurance policyholder in France, the surviving spouse, who in the meantime has moved to the south of France, will regain control over the life insurance policy until their death and when the policy is redeemed each of the children will then receive equal shares of the insurance proceeds.

What tax will their children pay?

As the premiums were paid before the couple turned 70, when they die all the beneficiaries will be subject to a sui generis tax (article 990 I of the General Tax Code, GTC). They will benefit from a tax allowance that may be as high as €152,200 per beneficiary.

It should also be noted that for deaths occurring after 31 July 2011, the 20% levy will be due if:

At the time of death the beneficiary is resident for tax purposes in France within the meaning of article 4B of the GTC and that this was true for at least six of the ten years preceding death.

Or if the policyholder, at the time of their death, is resident for tax purposes in France within the meaning of the same article 4B, which is true in our case.

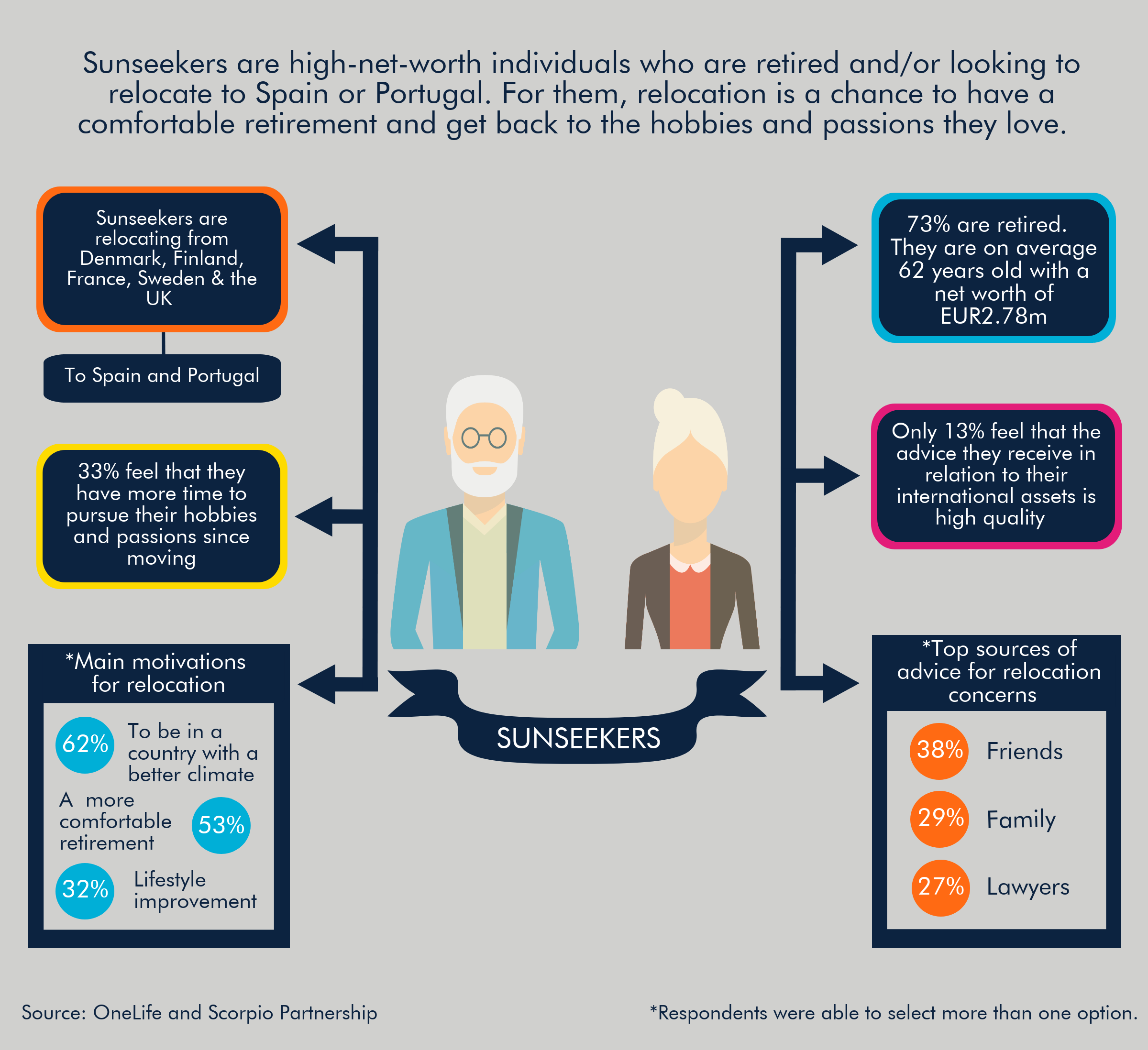

- For Jean, who lives in Sweden and is 30 years old

According to Swedish regulations no inheritance tax applies, Jean simply has to pay the tax due in France.

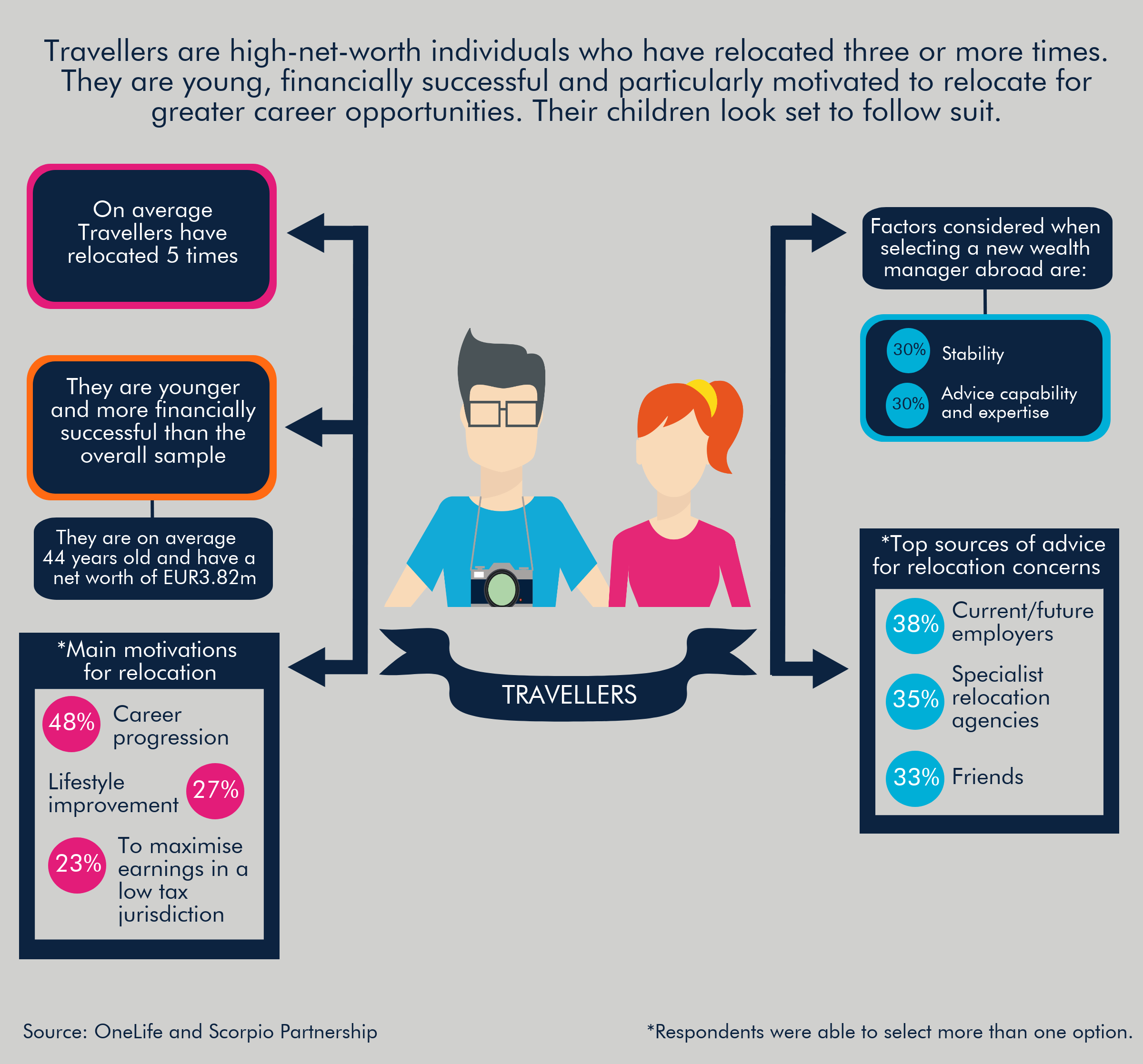

- For Paul who lives in Portugal and is 25 years old

According to Portuguese law, no taxation will be applied to Paul who will have to pay only the French tax.

- For Jeanne who lives in Belgium and is 20 years old

According to Belgian legislation, insurance policies may or may not be liable for inheritance tax; it all depends on the construction of the policy.

For Jeanne, inheritance tax will apply, the rate of which varies depending on the region in which she lives (article 8 of the Inheritance Code).

Apart from the degree of kinship, the value of the estate and the residence for tax purposes of the deceased will also play a role.

Onelife can provide you with tailor-made solutions adapted to your personal situation and your requirements to enable you to plan for the passing on of your estate or simply manage your assets.

Article by  Nora Belarbi, Legal Advisor at OneLife

Nora Belarbi, Legal Advisor at OneLife